StockEmotions: Discover Investor Emotions for Financial Sentiment Analysis and Multivariate Time Series

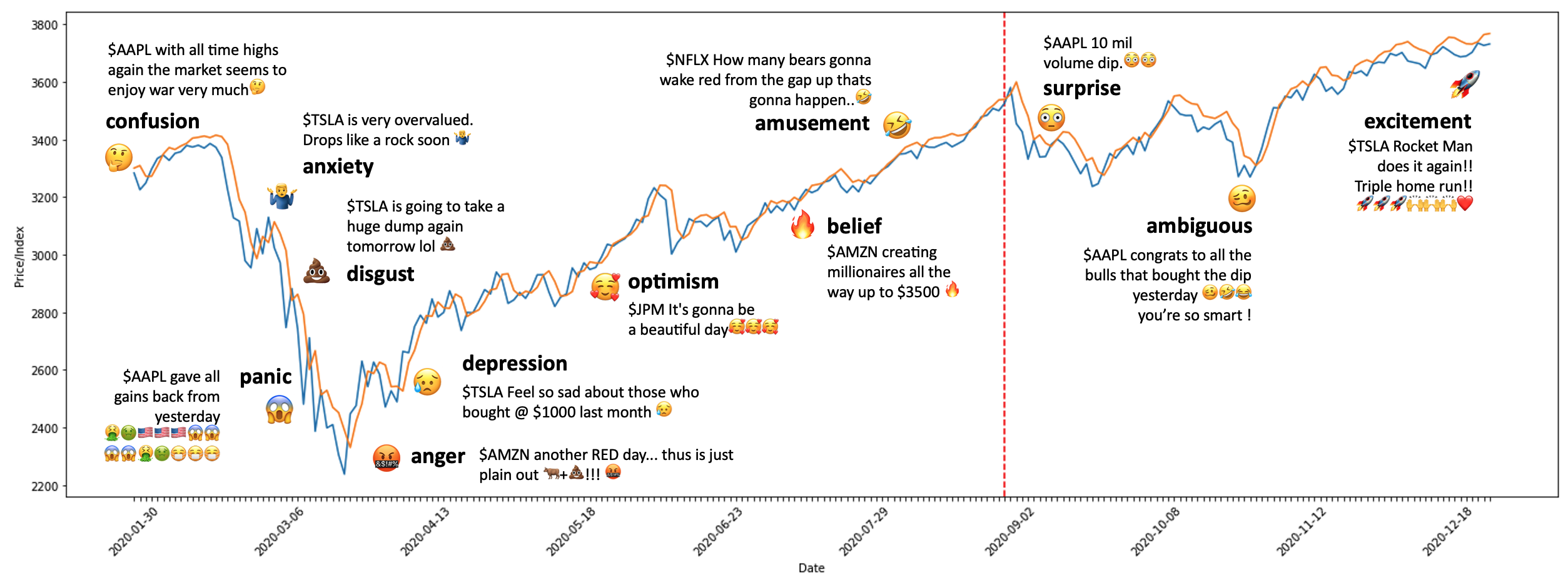

There has been growing interest in applying NLP techniques in the financial domain, however, resources are extremely limited. This paper introduces StockEmotions, a new dataset for detecting emotions in the stock market that consists of 10,000 English comments collected from StockTwits, a financial social media platform. Inspired by behavioral finance, it proposes 12 fine-grained emotion classes that span the roller coaster of investor emotion. Unlike existing financial sentiment datasets, StockEmotions presents granular features such as investor sentiment classes, fine-grained emotions, emojis, and time series data. To demonstrate the usability of the dataset, we perform a dataset analysis and conduct experimental downstream tasks. For financial sentiment/emotion classification tasks, DistilBERT outperforms other baselines, and for multivariate time series forecasting, a Temporal Attention LSTM model combining price index, text, and emotion features achieves the best performance than using a single feature.

PDF AbstractCode

Colab

Colab

Datasets

Introduced in the Paper:

StockEmotions

StockEmotions