LSTM-MSNet: Leveraging Forecasts on Sets of Related Time Series with Multiple Seasonal Patterns

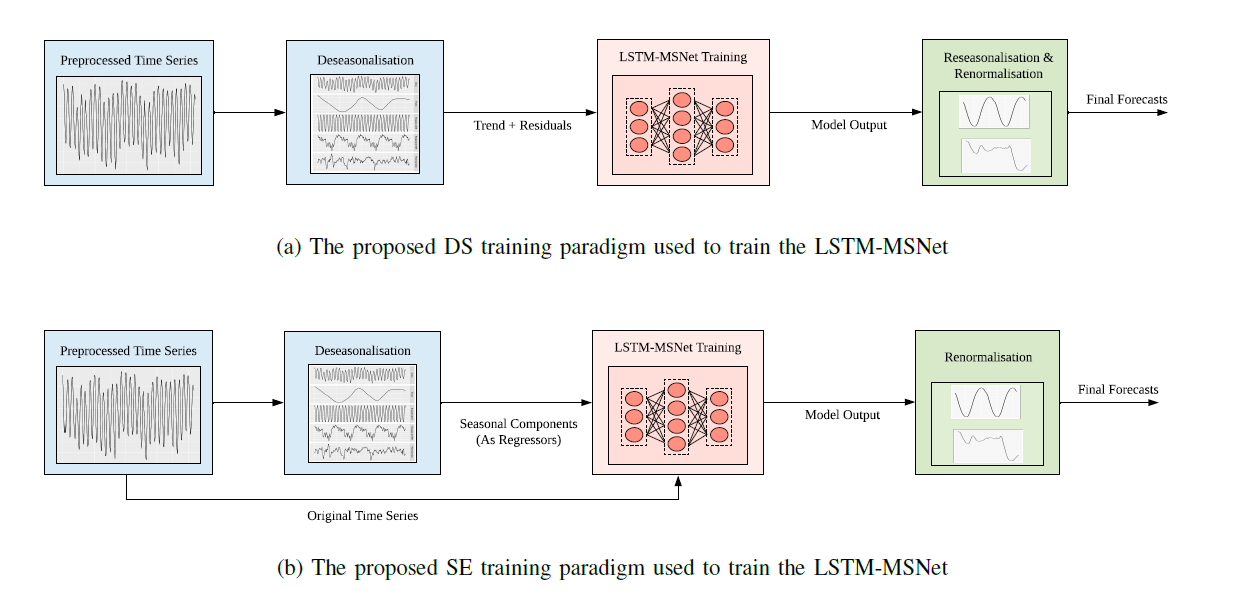

Generating forecasts for time series with multiple seasonal cycles is an important use-case for many industries nowadays. Accounting for the multi-seasonal patterns becomes necessary to generate more accurate and meaningful forecasts in these contexts. In this paper, we propose Long Short-Term Memory Multi-Seasonal Net (LSTM-MSNet), a decomposition based, unified prediction framework to forecast time series with multiple seasonal patterns. The current state of the art in this space are typically univariate methods, in which the model parameters of each time series are estimated independently. Consequently, these models are unable to include key patterns and structures that may be shared by a collection of time series. In contrast, LSTM-MSNet is a globally trained Long Short-Term Memory network (LSTM), where a single prediction model is built across all the available time series to exploit the cross series knowledge in a group of related time series. Furthermore, our methodology combines a series of state-of-the-art multiseasonal decomposition techniques to supplement the LSTM learning procedure. In our experiments, we are able to show that on datasets from disparate data sources, like e.g. the popular M4 forecasting competition, a decomposition step is beneficial, whereas in the common real-world situation of homogeneous series from a single application, exogenous seasonal variables or no seasonal preprocessing at all are better choices. All options are readily included in the framework and allow us to achieve competitive results for both cases, outperforming many state-of-the-art multi-seasonal forecasting methods.

PDF Abstract

M4

M4