Gradient boosting for convex cone predict and optimize problems

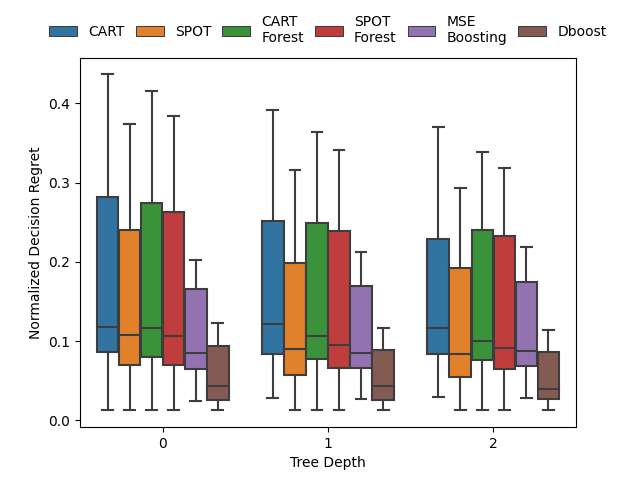

Prediction models are typically optimized independently from decision optimization. A smart predict then optimize (SPO) framework optimizes prediction models to minimize downstream decision regret. In this paper we present dboost, the first general purpose implementation of smart gradient boosting for `predict, then optimize' problems. The framework supports convex quadratic cone programming and gradient boosting is performed by implicit differentiation of a custom fixed-point mapping. Experiments comparing with state-of-the-art SPO methods show that dboost can further reduce out-of-sample decision regret.

PDF AbstractCode

Tasks

Datasets

Add Datasets

introduced or used in this paper

Results from the Paper

Submit

results from this paper

to get state-of-the-art GitHub badges and help the

community compare results to other papers.

Methods

No methods listed for this paper. Add

relevant methods here