A Dual-Stage Attention-Based Recurrent Neural Network for Time Series Prediction

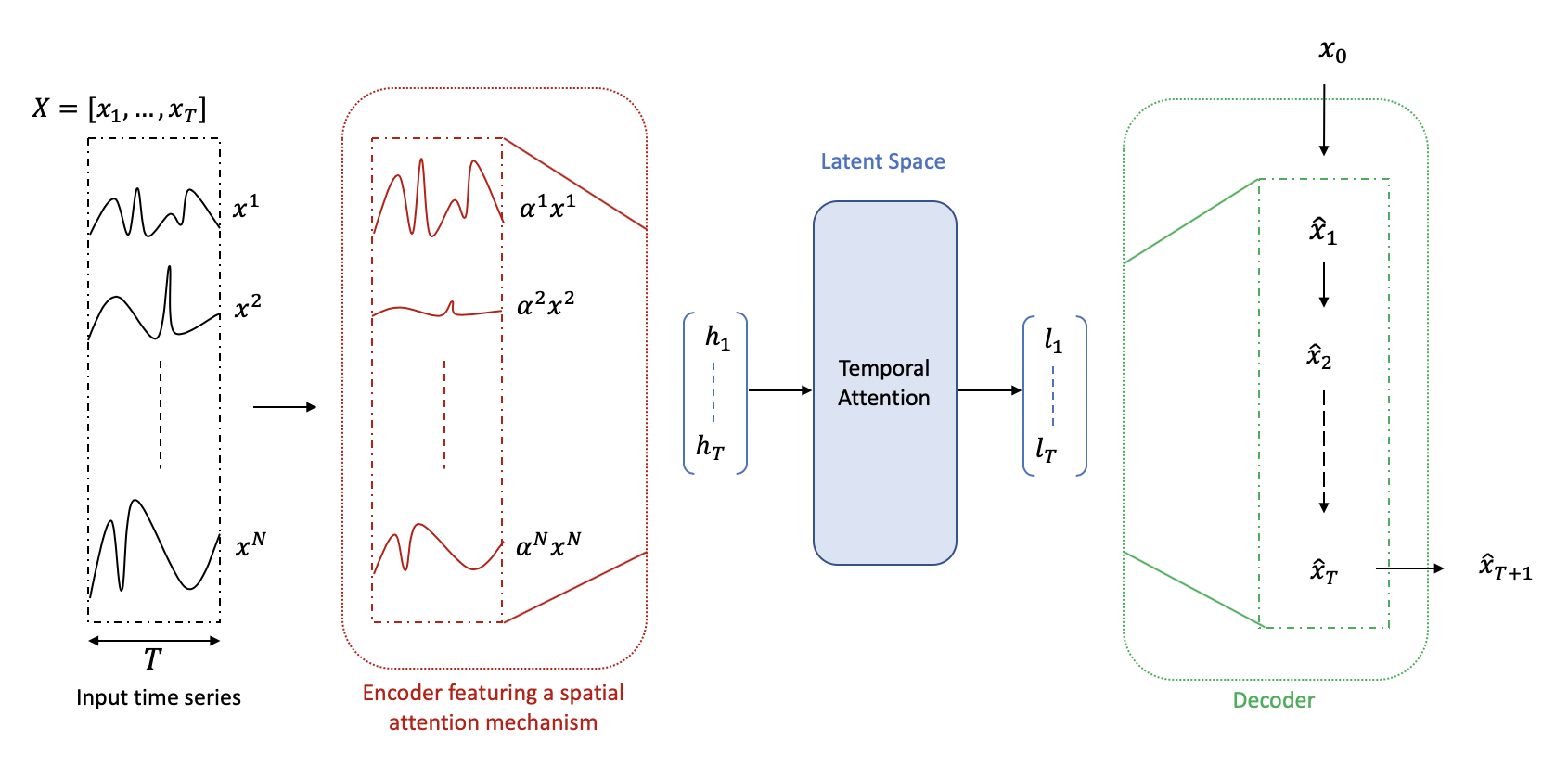

The Nonlinear autoregressive exogenous (NARX) model, which predicts the current value of a time series based upon its previous values as well as the current and past values of multiple driving (exogenous) series, has been studied for decades. Despite the fact that various NARX models have been developed, few of them can capture the long-term temporal dependencies appropriately and select the relevant driving series to make predictions. In this paper, we propose a dual-stage attention-based recurrent neural network (DA-RNN) to address these two issues. In the first stage, we introduce an input attention mechanism to adaptively extract relevant driving series (a.k.a., input features) at each time step by referring to the previous encoder hidden state. In the second stage, we use a temporal attention mechanism to select relevant encoder hidden states across all time steps. With this dual-stage attention scheme, our model can not only make predictions effectively, but can also be easily interpreted. Thorough empirical studies based upon the SML 2010 dataset and the NASDAQ 100 Stock dataset demonstrate that the DA-RNN can outperform state-of-the-art methods for time series prediction.

PDF Abstract

Colab

Colab